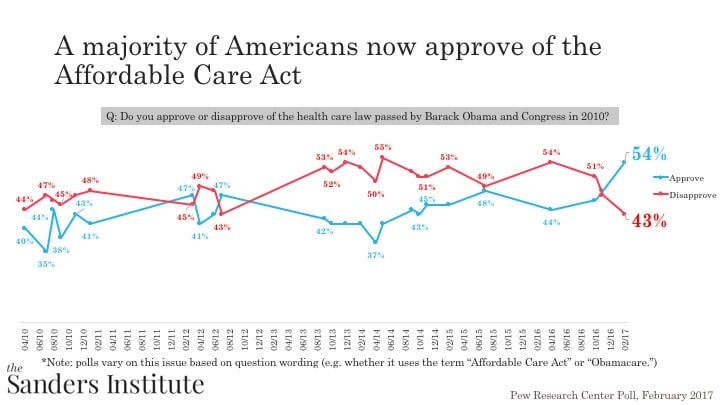

Opinions of the Affordable Care Act (also known as Obamacare) have fluctuated since it was first signed into law in 2010.

It has been the topic of many high-profile court cases and was a key issue in the 2016 Presidential campaign. For the most part, at least a plurality of the American public has disapproved of the ACA since its passage into law. The two outliers are during 2012, which coincides with the 2012 presidential election, and right now. In fact, more Americans approve of the ACA right now (54%) than they ever have.

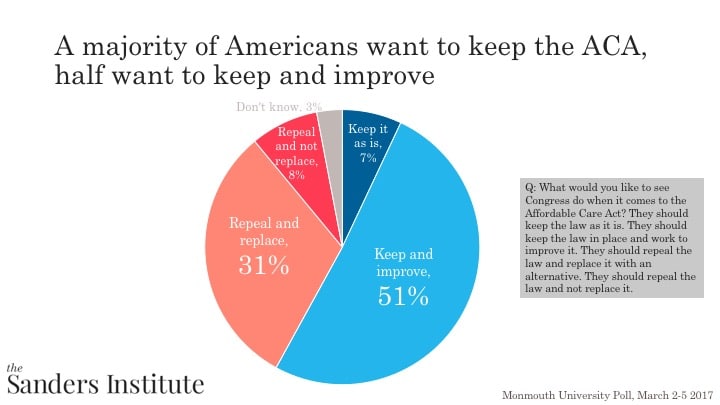

When asked what they would like Congress to do with the law, almost six in ten (58%) Americans want to either keep the law as it is (7%) or keep the law and improve it (51%). In contrast, four in ten (39%) Americans would like to either repeal and replace the law (31%) or repeal with no replacement (8%).

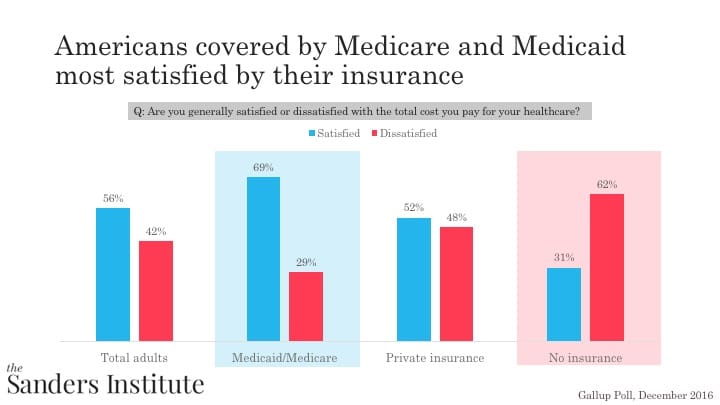

Ultimately, over half (56%) of Americans are satisfied with the cost they pay for insurance. However, the type of insurance is a strong determinant of satisfaction – seven in ten (69%) of individuals on the government programs Medicare and Medicade are satisfied with the cost they pay for insurance, while half (52%) those on private insurance are satisfied and only three in ten (31%) of those without insurance are satisfied.

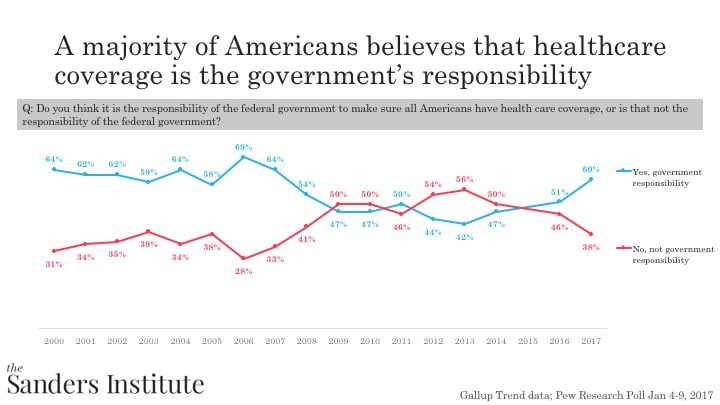

Opininons about whether healthcare coverage is the government responsibility have fluctuated over the years: from 2000 to 2008, a majority of Americans believed that healthcare coverage is the government’s responsibility. Between 2009 and 2016 opinions fluctuated. However, since 2016 there has been a sharp spike in the number of individuals who think it is the government’s responsibility (60% currently).

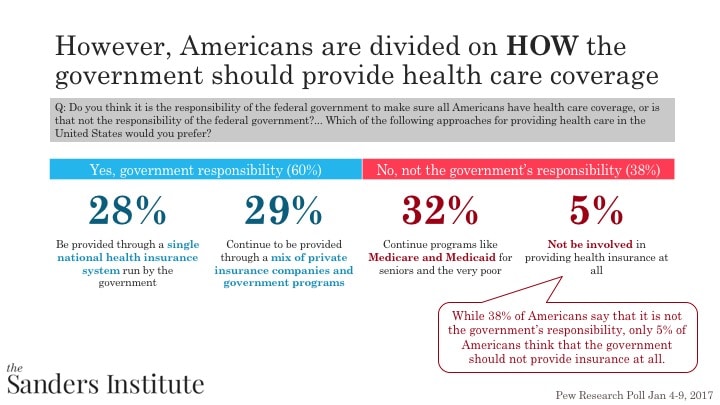

When asked to elaborate about how the government should or should not provide health care coverage, Americans are divided. When looking at those who said that healthcare coverage is the government’s responsibility, Americans are divided half and half. 28% of Americans think that the government should provide healthcare through a single payer system while 29% think that the government should provide healthcare through a mix of private insurance companies and government programs. In contrast, when we look at those who think that it is not the government’s responsibility to provide health care (38%), most want to maintain current programs like Medicaid and Medicare (32% of Americans). In fact, only 5% of Americans would think that the government should not be responsible for healthcare at all.