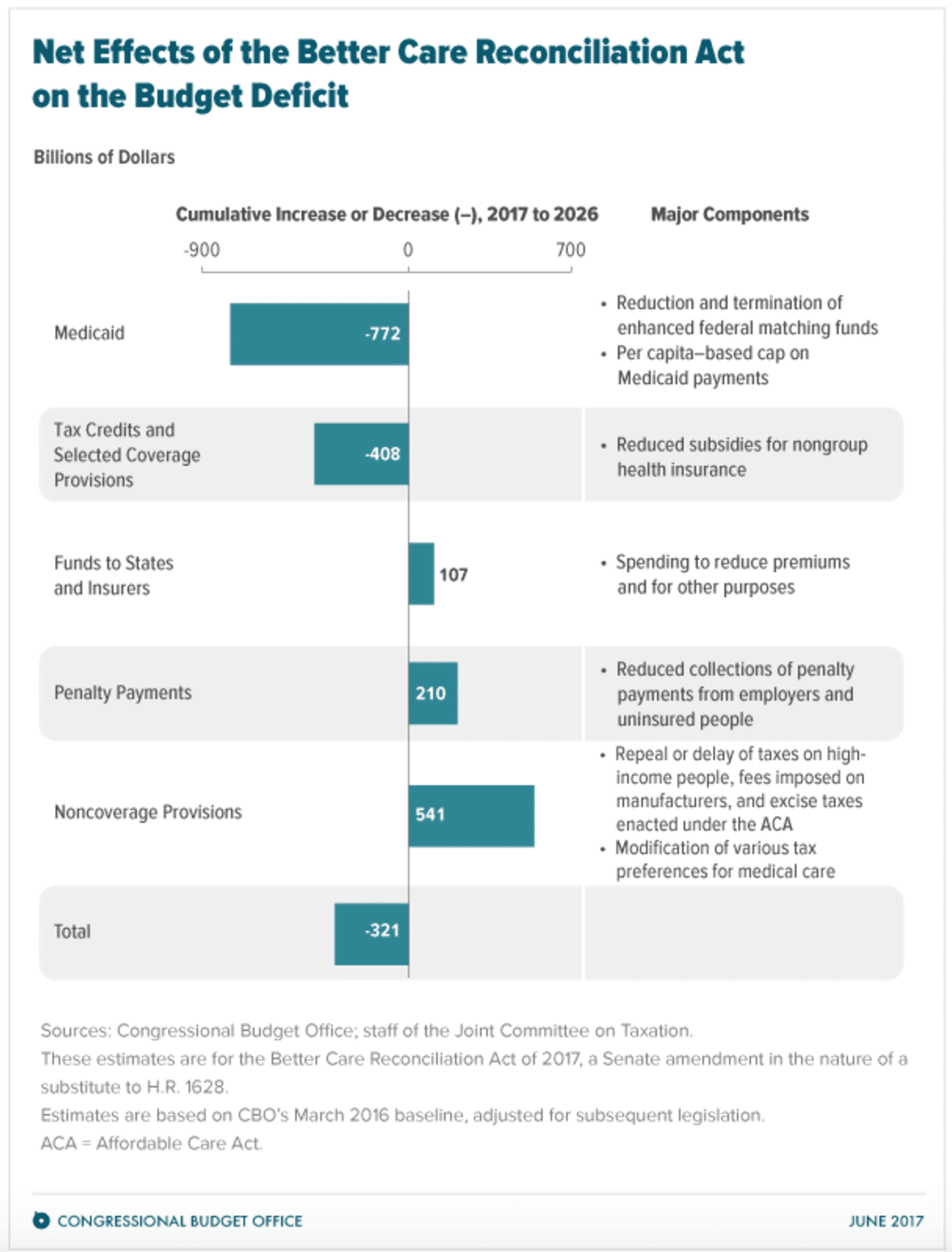

US health care costs are out of sight, more than $10,000 per person per year, compared with around $5,000 per person in Canada, Germany and France. Obamacare expanded coverage without controlling costs. The Republican plan would ruthlessly and cruelly limit coverage without controlling costs.

Of the two options, Obamacare is vastly more just. The Republican plan is ghastly. But America has a much better choice: health for all at far lower costs.

This might seem like an out-of-reach goal or a political slogan, but it is neither. Every other rich country uses the same medical technology, gets the same or better health outcomes, and pays vastly lower sums.

Why the disparity? Health care in America is big business, and in America big business means big lobbying and big campaign contributions, the public interest be damned.

Health care is our biggest economic sector, far ahead of the military, Wall Street and the auto and tech industries. It is pushing 18% of national income, compared with 10% to 12% of national income in the other high-income countries.

In line with its economic size, it ranks first in total lobbying, with a recorded $152 million in lobbying spending in 2017 and an estimated $273 million in federal campaign contributions in the 2016 election cycle, divided roughly equally between the parties.

Both parties have therefore ducked the hard work of countering the health care sector’s monopoly power. Health care spending is now at $10,000 per person per year, roughly twice or more the total of other high-income countries, or a staggering $3.25 trillion a year.

We should aim to save at least $1 trillion in total annual outlays, roughly $3,000 per person per year, through a series of feasible, fair and reasonable measures to limit monopoly power. Our system would look a lot more like that of the other more successful and less expensive nations.

Here’s a 10-point plan Congress should consider.

First, move to capitation for Medicare, Medicaid and the tax-exempt private health insurance plans. Under capitation, hospitals and physician groups receive an annual “global budget” based on their patient population, not reimbursement on a fee-for-service basis.

Second, limit the compensation of hospital CEOs and top managers. The pay of not-for-profit hospital CEOs and top managers, for example, could be capped at $1 million per year.

Third, require Medicare and other public providers to negotiate drug prices on a rational basis, taking account of research and development incentives and the manufacturing costs of the medicines.

Fourth, use emergency power to override patents (such as compulsory licensing of patent-protected drugs) to set maximum prices on drugs for public health emergencies (such as for HIV and hepatitis C).

Fifth, radically simplify regulatory procedures for bringing quality generic drugs to the market, including through importation, by simplifying Food and Drug Administration procedures.

Sixth, facilitate “task shifting” from doctors to lower-cost health workers for routine procedures, especially when new computer applications can support the decision process.

Seven, in all public and private plans, cap the annual payment of deductibles and cost-sharing by households to a limited fraction of household income, as is done in many high-income countries.

Eight, use part of the annual saving of $1 trillion to expand home visits for community-based health care to combat the epidemics of obesity, opioids, mental illness and others.

Nine, rein in the advertising and other marketing by the pharmaceutical and fast-food industries that has created, alone among the high-income world, a nation of addiction and obesity.

Ten, offer a public plan to meet these conditions to compete with private plans. Medicare for all is one such possibility.

There really no mystery to why America’s health industry needs a drastic corrective.

Visit the website of your local not-for-profit hospital system. There’s a good chance the CEO will be earning millions per year, sometimes $10 million or more. Or go to treat your hepatitis C with Gilead drug Sofosbuvir. The pills list for $84,000 per 12-week dose, while their production cost is a little over $100, roughly one-thousandth of the list price. Or go in for an MRI, and your hospital might have an $8,000 billable price for a procedure that costs $500 in a discount clinic outside your provider network.

All of these are examples of the vast market power of the health care industry. The sector is designed to squeeze consumers and the government for all they’re worth (and sometimes more, driving many into bankruptcy).

As a result, the sector is awash in profits and compensation levels, and the stock prices of the health care industry are soaring. In the meantime, human and financial resources are pulled away from low-cost (but also low-profit) disease prevention, such as low-cost community health workers and wellness counselors who work within the community, including household visits.

The health care sector is a system of monopolies and oligopolies — that is, there are few producers in the marketplace and few limits on market power. Government shovels out the money in its own programs and via tax breaks for private plans without controls on the market power. And it’s getting worse.

Every other high-income country has solved this problem. Most hospitals are government-owned, while most of the rest are not for profit, but without allowing egregious salaries for top management. Drug prices are regulated. Patents are respected, but drug prices are negotiated.

None of this is rocket science. Nor is the United States too dumb to figure out what Canada, the UK, France, the Netherlands, Germany, Japan, Sweden, Norway, Denmark, Finland, Austria, Belgium, Korea and others have solved. The problem is not our intelligence. The problem is our corrupt political system, which caters to the health care lobby, not to the needs of the people.